According to a report from commercial real estate advisor CBRE Hotels, investment into European hotels reached €3.7 billion in the first quarter of the year, representing the second-largest deal volume recorded in any first quarter in the last decade. This achievement was in spite of transaction volumes falling 30 percent compared to Q1 2015.

During a record year for hotel investment in 2015, the asset class grew its share of total European real estate investment to 8 percent. Figures for the quarter also show that hotels have retained the 8 percent share and levels of liquidity relative to other sectors has not abated.

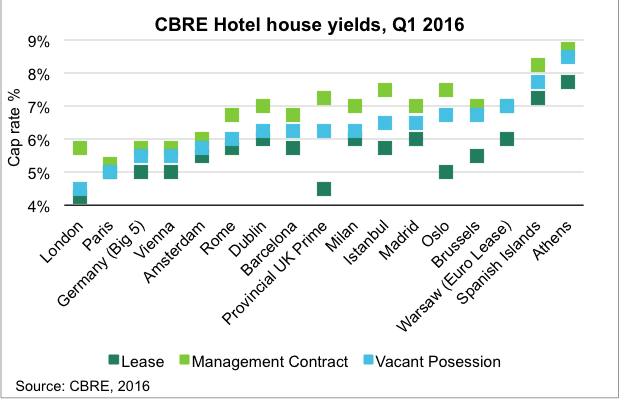

“While hotel yields in markets such as London, Paris, regional U.K. and the top five German cities are low and stable relative to other key European markets, hotel profitability principally continues to track a trajectory of growth, highlighting scope for the continued increase of capital values on operational investments,” Joe Stather, information and intelligence manager EMEA at CBRE Hotels said in a statement. “Notably, Germany has the highest ratio of hotel stock encumbered by an operational lease; some of which will likely satisfy the escalating quantum of institutional capital targeting core real estate and therefore add further to the country’s 2016 transaction volume.”

Country by Country

Germany is fast becoming a key investment market in Europe, offering consistently high levels of liquidity. Achieving double-digit growth (+17 percent) in Q1 2016 with transactions reaching €750 million means the market could take the long-standing mantle from the U.K., which has dominated the investment volumes in the last decade.

The U.K.’s hotel transaction turnover, on the other hand, declined by 58 percent in Q1 year-over-year, as the Brexit’s impact on the hotel investment market there has left some investors waiting to see the outcome of the impending referendum. Despite this, many players have remained active and have attempted to capitalize on potentially less competitive sales process. A shortage of stock is also having an impact on the level of hotel investment in the U.K., considering the numbers of bulky portfolios brought to the market in 2015, which are unlikely to trade again in the coming months. International visitation is expected to grow by 3 percent year-over-year, but with a 2016 confirmed room-supply increase of 5 percent, some of the city submarkets will undoubtedly come under pressure to sustain 2015 levels of performance.

Last month, CBRE’s ‘Heading for the Exit?’ report predicted that if the U.K. votes to remain in the EU, business as usual—including "a glut of investment decisions" can be expected for the immediate aftermath. "However, should Britain choose to leave we can expect a ‘long goodbye’ stretched out over two years or more and lingering uncertainty which would ultimately reduce investment in the longer term. A poll of CBRE investor clients in February 2016 found that 73 percent believe the UK would be a worse place to invest should the country vote to exit."

Italy saw a significant uptick in Q1 2016 investment performance with deal volumes rising 131 percent year-over-year. While the country’s economy is still fragile, hotel performance is going strong across most key markets, coupled with a steady contraction of yields and thus recovery of capital values. On this basis, it is likely that more products (particularly distressed) will be readied for sale in 2016 and while some of the outlined challenges will remain, strong return prospects undoubtedly exist for well-advised investors.

France saw a Q1 decline in hotel transaction volumes of -43 percent year-over-year to €206 million, which can be partially attributed to the November 2015 terrorist attacks in Paris. While sentiment suggests that buyer appetite has not subsided, owners are reluctant to sell based on present values reflecting the associated dip in operating performance. Data shows a slowing of declining room revenues in Paris only four months post the November attacks, highlighting Paris’ strength and resilience as a destination.

The Belgian hotel market achieved impressive transaction volume growth for Q1 2016 (+80 percent), but the terrorist attacks in March hampered growth as initial figures show a -17-percent year-over-year market decline in total room revenue for the one month alone. Brussels’ relatively high business mix, in terms of demand make-up, may help the recovery of the market. In the report, CBRE claims that corporate travelers "generally exhibit less sensitivity to such atrocities compared to the leisure sector."