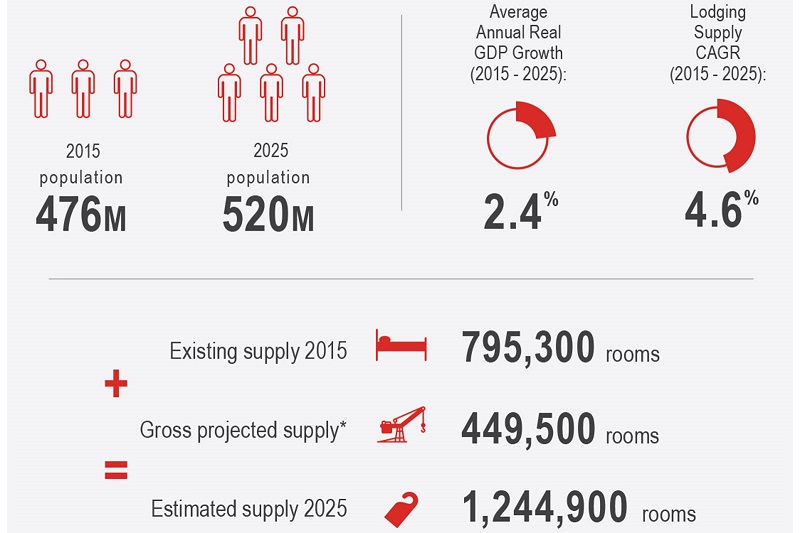

A new report from JLL indicates that the Latin American lodging market is undergoing "a significant economic transformation" in spite of economic pressures. Sustained investment in existing and new hospitality projects is poised to fuel lodging demand to support supply growth through 2025.

The firm’s paper, "Impact of Economic Transformation on Latin America’s Lodging Industry," includes an analysis of hotel supply and demand in six Latin American countries: Mexico, Chile, Argentina, Brazil, Colombia and Peru. Combined, these countries account for more than 75 percent of the total population in Latin America and approximately 85 percent of the region’s gross domestic product.

According to the research, the economic outlook of the world’s emerging countries is "less optimistic" than it was a few years ago. Decreases in commodity prices, particularly oil and gas, currency devaluations and shifting investor sentiment has impacted economic growth. Despite the region’s impediments to growth, which is being experienced unevenly across the six targeted countries, the broader transformation toward more open, services-oriented economies continues largely unabated.

Top Takeaways

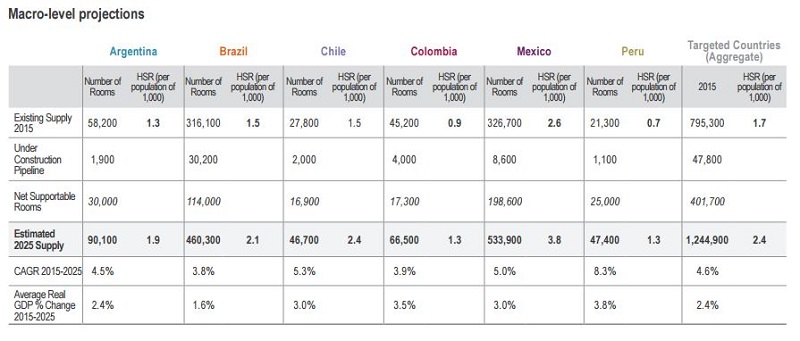

Mexico is the most advanced country in terms of its lodging market with an existing hotel supply ratio (a measure of the estimated relevant hotel rooms in a country per 1,000 inhabitants) of 2.6. A steady volume of business, tourism and infrastructure investment over the next decade will increase its hotel supply ratio to 3.8.

Chile, generally regarded as one of the region's most stable economies, is expected to see a 5.3-percent increase in supportable supply, bringing in an estimated 46,700 quality hotel rooms by 2025.

Argentina has the third-largest existing supply of quality hotel rooms, and a significant number of hotel projects are expected to develop in the next two to three years. Buenos Aires presents the highest growth opportunity with 14,000 new rooms expected over the next 10 years, although an anticipated uptick in agro-industrial investment and pent-up demand is expected to support new supply in the provinces as well.

Brazil, which has the largest and most diversified economy in Latin America, has received significant investment over the past decade. This, combined with two global events–the 2014 FIFA World Cup and 2016 Summer Olympic Games–has already propelled considerable investment in the lodging sector, with more than 30,000 rooms currently under construction.

Colombia has also experienced substantial supply increases driven by tourism and general economic growth and special tax incentives. While the petroleum sector has suffered, Colombia is expected to garner a steady amount of investment volume over the next decade as it continues to emerge as an attractive business and tourist destination.

Coming off a comparatively small base of existing stock, Peru shows the highest growth rate among the profiled countries, with an 8.3-percent compounded annual growth rate in quality lodging supply over the next decade.

JLL also noted the "proliferation" of branded hotels by both regional and global brands across all of the countries. The vast majority of new hotels added between 2012 and 2015 as well as projects in the current pipeline are branded. Brand changes and conversions from independent properties were also prevalent during the period, with approximately 11,000 room conversions in Brazil and 10,000 in Mexico. The trend toward branding is expected to accelerate with the addition of new hotels and the removal of obsolete product, and by 2025 branded assets are expected to surpass independent products.

The paper, "Impact of Economic Transformation on Latin America’s Lodging Industry," was prepared by JLL’s Hotels & Hospitality Group and supported by Wyndham Hotel Group, AccorHotels, Hilton Worldwide and Interstate Hotels & Resorts. Information was derived from a number of sources, including Smith Travel Research, national hotel associations, online travel agencies, JLL’s proprietary databases and Financial Times Confidential Research. The full report is available at www.jll.com/latam-whitepaper.