With hotels in both London and the UK's regional markets set for a strong 2017, it would seem that a rising tide is floating all of the country's boats.

Not quite: The latest Hotel Bulletin Q4 2016 from HVS, AlixPartners, STR and AM:PM has found a growing divide in the UK’s hotel sector between the performance of leisure-based hotels and primarily business-orientated properties. At the same time, while some cities are seeing improvements in revenue per available room and other primary indicators, other major cities in England, Scotland and Wales alike are seeing steep declines.

Business vs. Leisure

Hotels in cities with a more developed tourism industry performed noticeably better in the last quarter of 2016 as a result of the weaker pound attracting foreign tourists and locals choosing staycations.

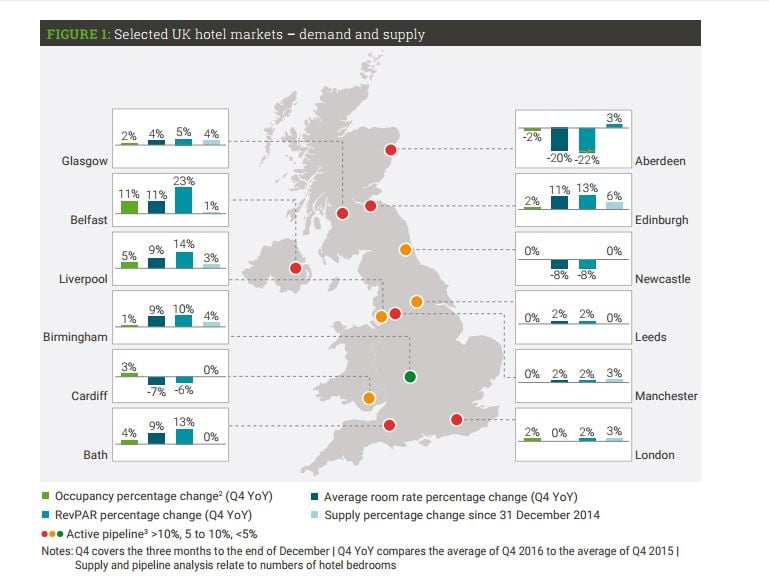

Belfast, Northern Ireland, for example, saw RevPAR growth of 23 percent during the final quarter of 2016 following significant investment in the city as a tourist destination. Liverpool, England’s hotels reported growth of 14 percent during the same period, while Edinburgh, Scotland, and Bath, England, both reported 13 percent growth in RevPAR.

At the same time, hotels in Newcastle, England, saw an 8-percent decline in RevPAR during Q4 2016, and Aberdeen, Scotland, a 22-percent decline on the back of the falling oil market, while in Cardiff, Wales, RevPAR dropped 6 percent.

Hotels in London saw a "modest" 2-percent increase in both RevPAR and occupancy, while average daily rate in the city remained static. Occupancy in London’s hotel sector had shown a decline for the previous seven quarters.

“As the most popular tourist city, London is particularly well placed to attract more visitors and benefit from the weaker pound but growth was offset by the potential of corporate decline,” HVS chairman Russell Kett said in a statement. “London may see a further decline in corporate bookings because of depressed [gross domestic product] growth, particularly if threats made by several large companies to move staff out of the country come to fruition.”

Supply and Demand

The pound finished 2016 16 percent down on the dollar compared to before the Brexit result was announced. Belfast, Bath, Liverpool and Edinburgh benefited from a weaker pound, making UK vacations cheaper for foreign visitors and staycations more attractive to cost-conscious locals.

By contrast, cities more traditionally focused on corporate visitors, like Newcastle, Aberdeen and Glasgow, Scotland, have reported falling RevPAR compared with last year.

The average Q4 2016 RevPAR growth over the 12 cities reviewed in this bulletin was 4 percent. This modest figure disguises performance polarity, with RevPAR growth ranging from 23 percent in Belfast to a fall of 22 percent in Aberdeen.

The steady increase in the UK’s hotel supply continued with the addition of 14,600 hotel bedrooms during 2016—a net increase of 1.7 percent when closures are taken into account. Forecasts estimate that 2017 will see supply growth of 3.3 percent. London shows the strongest annual growth in hotel bedrooms, while the UK’s regions average a net supply gain of 1 percent.

Sector Strength

The budget sector makes up 47 percent of the UK’s active pipeline as Premier Inn and Travelodge continue their aggressive expansion plans. The two brands account for nearly 70 percent of budget bedrooms opened in 2016. Around 30 percent of the active pipeline are four-star hotels, 10 percent are apartments and 9 percent are five-star properties.

“Budget brands now account for 25 percent of all hotel bedrooms in the UK, while the main casualties have been the two- and three-star properties. It’s difficult to envisage this trend changing for the foreseeable future,” Kett said.

Uncertain Times

Transaction values in the last quarter of 2016 totaled £0.6 billion, significantly lower than the £2 billion of transactions recorded in the same quarter of 2015. Overall transaction levels in 2016 (£2.4 billion) were less than half that of the previous year's record level (£5.3 billion).

The low level of transactions reflects the sentiment in the mergers-and-acquisitions market as a whole, the report claimed, noting that M&A activity in the UK was 55 percent lower than in 2015. This could be credited to "significant levels of uncertainty" in the market during late 2016—undertainty over what form Brexit will take and how the U.S. political situation will affect the global economy.

This uncertainty is expected to continue in 2017—but there are signs that investors are returning to the hotel market as performance continues to be robust. UK real estate remains an attractive asset class for domestic and international investors, the report claimed, and certain sectors (such as serviced apartments) that demonstrate strong fundamentals and a growth opportunity are expected to generate significant investment appetite in the medium term.

Download the Hotel Bulletin: Q4 2016 here.