JLL’s Hotel Investment Outlook report predicts that global hotel real estate transactions this year will likely match last year’s $60 billion. But if 2016 was “a year of resets and changes,” 2017 will be a “year of stability and greater consistency for investment flows,” the report says.

A Year of Shifts

Last year marked a year of shifts, Lauro Ferroni, global head of research at JLL told HOTEL MANAGEMENT, primarily in terms of who the big dealmakers were at the table. “During 2015, so much was driven by purchases of private equity funds,” he said. “That’s where we saw a big reset and a lot of changes in 2016. It was the year of the institutional investor.”

Transaction structures continue to evolve, and the role and clout of private-equity funds is changing. Institutional investors—some tied to pension funds or, as in China, connected to large insurance companies—pulled ahead of private-equity investors last year, and the trend is likely to continue. “As we get to a hotel market that continues to mature in terms of having more years of growth under our belts, that’s when investment groups like investment funds that have a shorter-hold horizon take a step back, assess where they are, and the kind of money they’re deploying,” Ferroni said. “They want to be sure they’re early enough in the cycle so they can potentially dispose of real estate while the fundamentals are growing. When it comes to institutional buyers, since they have a longer-hold horizon, they don’t have to be quite as focused on the exact timing of the acquisition. They were very active last year and, frankly, they’re seeing pressure with groups to deploy money and make deals happen.”

A lot of the deals, Ferroni said, are large portfolio transactions. “Perhaps one difference is that, historically, we’ve seen private equity groups getting portfolios of select-service hotels, while institutional investors, for the most part, are centered around full-service hotels,” he said.

Transactions in 2017 will largely be driven by funds reaching the end of their hold period and the subsequent restructuring of portfolios, rather than high-income growth, the report said. “That will be a big force throughout the year,” Ferroni said. Investors who have purchased portfolios or individual assets will start deciding which properties are core to their strategy and which they want to drop, he predicted.

Outbound Investment

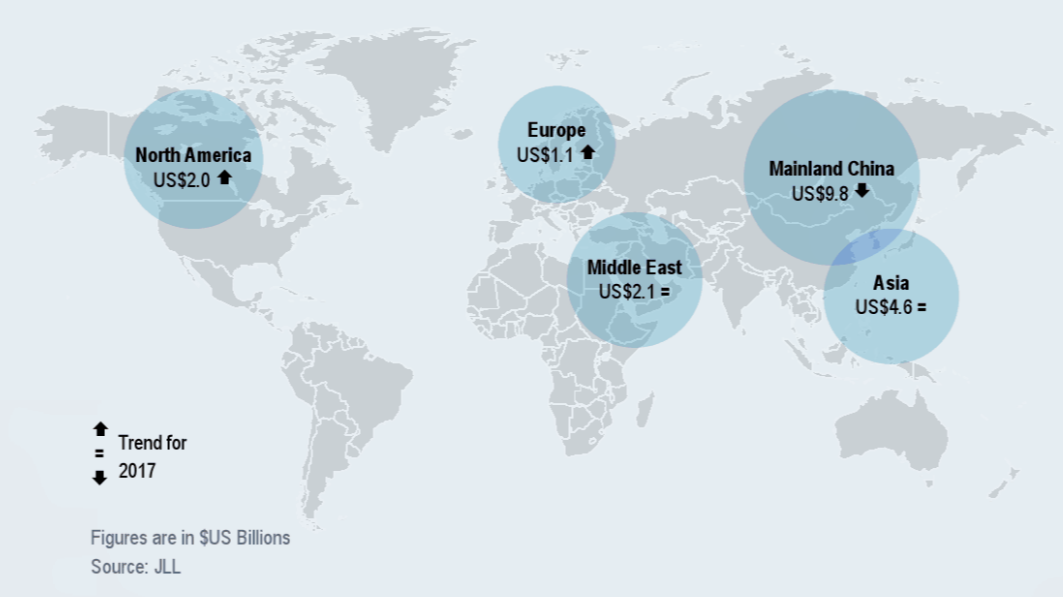

The proportion of investments funded by off-shore capital reached an all-time record of 33 percent in hotel deals. In 2017, with more uncertainty regarding how capital from mainland China will shape up, JLL expects this proportion to decrease, but remain in line with the recent multi-year average.

Last year, North America overtook Europe as the largest destination for inbound capital, attracting nearly $14 billion from overseas investors. It should not be a surprise that investors from mainland China were the largest outbound force, followed by other Asian countries.

Capital from the Middle East is down "greatly" from recent annual averages, the report said, due to economic woes in oil-producing countries. As such, their outbound activity in 2017 is expected to be flat.

American-based private equity funds were largely absent abroad for most of 2016, but started making bolder and more frequent plays in Europe towards the end of 2016. JLL expects this trend to continue now that some shock surrounding the EU referendum has subsided; Spain will be most favoured but we expect selected plays in the UK as well.

Outbound flows from Europe will continue to rise, driven by institutional investors targeting high-profile leased assets. Investors from Asia, outside of mainland China, will continue to feature, with groups from South Korea and Singapore at the fore. Hong Kong-based buyers with capital connected to China stand to be active as well.

Top Markets

Investors will continue to pursue yield, and move into more secondary and tertiary markets, according to the report. Some markets where hotel performance has turned negative will see more stress in 2017, resulting in potential opportunities for buyers.

The EMEA region is expected to see growth in volumes from approximately $20.5 billion in 2016 to $22.5 billion in 2017. After a strong year underpinned by offshore buyers, the Americas are expected to remain flat at up to $31 billion. And Asia Pacific volumes are expected to hold steady at $8.5 billion in 2017.

Regional numbers can be tied to travel trends in 2016. Globally, international travel grew by 3 percent in 2016. Japan, South Korea, Vietnam, Spain, Portugal and Ireland recorded double-digit growth, while major gateways across the U.S. saw record visitor levels in 2016. At the same time, tourist arrivals in France, Belgium and Turkey were impacted due to terrorist attacks.

In Europe, Spain has become a success story after years of economic struggle. The growth in visitors—and, by proxy, in hotel demand—can be attributed both to its value and its safety. “It will be a big target in 2017,” Ferroni said. “Hotel purchases are well-priced and not too expensive. The market is expected to do well in terms of demand and volumes.”

The first half of the year saw relatively few deals in the UK while investors waited to see what would happen with the Brexit vote. Once the initial shock had passed, Ferroni said, business resumed as normal.

But the hotel industry, he noted, can change quickly, and a market that’s hot one week can be old news within a week. While political instability or terrorism can affect the performance and value of hotels in a specific region in the short term, once traveler confidence builds again, the numbers can turn around.

In the U.S., the stable outlook is the same in terms of dollar volume. “We expect to see more activity from domestic buyers,” Ferroni said. “We saw the highest proportion come in from offshore, with headline figures from China. That will probably slow down a bit with more restrictions.” REITs in the U.S. are poised to be more active, he said, and while some buyers will shift ground, the liquidity amount will be the same.

Take a look at the full report here.