Assuming U.S. revenue-per-available-room growth remains positive through year end, 2016 will mark the seventh consecutive year of RevPAR growth for the U.S. lodging sector. Considering the length of the current cycle as well as recent turbulence in the capital markets, many hotel investors have begun to ask whether RevPAR is nearing its cyclical peak. Since the national supply growth outlook remains relatively benign and lodging demand has historically been highly correlated with real GDP growth, the answer to this question likely hinges on the U.S. macroeconomic outlook.

Key measures of economic activity in the U.S. indicate that macroeconomic fundamentals remain strong. In 2015, real GDP increased 2.4 percent, compared to average annual growth of 2.1 percent thus far in the current recovery. Real growth in personal consumption expenditures accelerated from 2.7 percent in 2014 to 3.1 percent in 2015—the highest growth rate in 10 years. The seasonally adjusted unemployment rate has continued to decline fairly steadily throughout the past year, to 5 percent as of March 2016.

After slowing in 2014, house price appreciation accelerated in 2015. The S&P/Case-Shiller 20-City Composite Home Price Index registered 5.8 percent growth at year-end 2015. The University of Michigan Consumer Sentiment Index increased from an average monthly reading of 84.1 in 2014 to 92.9 in 2015.

However, a divergence between the strength of macroeconomic fundamentals in the U.S. and wavering sentiment in the financial markets has emerged during the past year, fueling worries that the U.S. economy is poised for a meaningful slowdown. Many of the concerns regarding the growth prospects for the U.S. economy appear to stem from five popular misconceptions:

1.

The stock market is a good indicator of the health of the U.S. economy.

Neither the scale nor the duration of stock market declines have always borne a close relationship with the state of the U.S. economy; negative year-over-year growth in equity prices has coincided with a recession only about half of the time in recent history. In the aftermath of the stock market crash in October 1987, the year-over-year decline in the monthly average for the S&P 500 Index ultimately troughed at nearly 20 percent in the summer of 1988, and the economy did not fall into recession. The stock market declined 19.6 percent between May and October 2011, only to be followed by years of economic expansion

2.

The Chinese economy is performing poorly and Chinese equity markets are in free fall.

Chinese equity markets have declined significantly since June 2015, but it is worth bearing in mind that pricing for publicly traded Chinese equities skyrocketed prior to then. Between early February and mid-June 2015, the Shanghai Composite Index rallied 68 percent. As of early April 2016, the index is down approximately 41 percent from its June 2015 peak. On balance, the Shanghai Composite Index has declined only 6 percent since the start of 2015 and has increased nearly 45 percent since the start of 2014.

3.

The United States is ‘the only’ economy that is performing well and greatly at risk given global economic weakness.

In addition to China, Mexico and the European Union have benefited from moderate growth in real GDP in recent quarters. As of Q4 2015, real GDP registered year-over-year growth of 2.5 percent in Mexico and 1.8 percent in the European Union. It is worth noting that the U.S. has a relatively closed economy with limited exposure to foreign demand. In the U.S., total exports account for approximately 13.5 percent of GDP, less than the corresponding shares for most other major economies.

4.

The decline in oil prices and appreciation of the U.S. dollar are strong net negatives with respect to the country’s economic growth prospects.

The appreciation of the U.S. dollar is a reflection of the U.S. economy’s strength. Although U.S. dollar appreciation tends to have a deleterious impact on exports growth, the U.S. economy’s limited reliance on exports insulates it from the potential boomerang impact of a strong dollar. While certain U.S. markets that have historically depended upon oil production for a sizable share of their economic output are now grappling with slower or negative growth in the wake of oil price declines, the overwhelming majority of U.S. markets have limited economic exposure to oil production. In 2014, oil and gas extraction accounted for just 1.4 percent of gross output by industry in the U.S.

5.

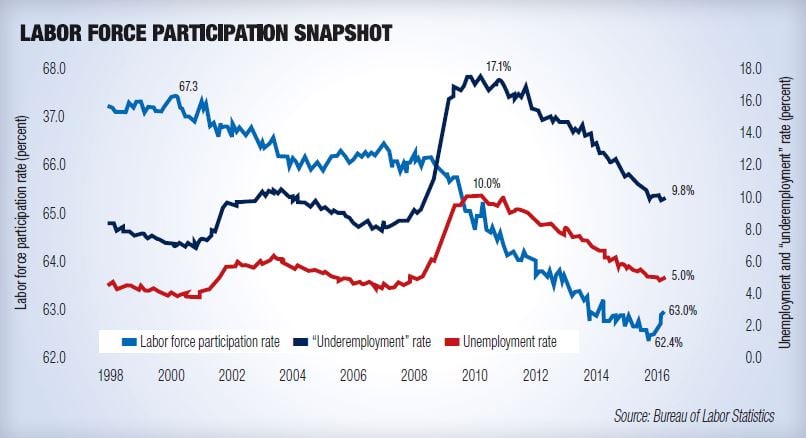

The improvement in the labor market is a total mirage; the only reason the official unemployment rate has declined is because the number of discouraged workers has increased.

In fact, an alternative measure of “underemployment,” which takes discouraged workers as well as part-time workers who would prefer full-time work into account, demonstrates substantial improvement in the labor market. Since peaking at 17.1 percent, the “underemployment” rate has declined to 9.8 percent as of March 2016. After declining steadily for years, the labor force participation rate has finally begun to inch up again in recent months, rising from 62.4 percent in September 2015 to 63 percent as of March 2016.