On July 31, a Bloomberg headline hit the wires with the claim that China was asking Anbang Insurance Group, one of the largest foreign owners of U.S. assets, specifically in the hospitality sector, to sell its overseas assets, including the Waldorf Astoria in New York.

The story did not name an actual source and has since been rebutted by Chinese officials. The China Insurance Regulatory Commission, as reported by the South China Morning Post, vehemently denied that it had pressed Anbang to divest its offshore assets.

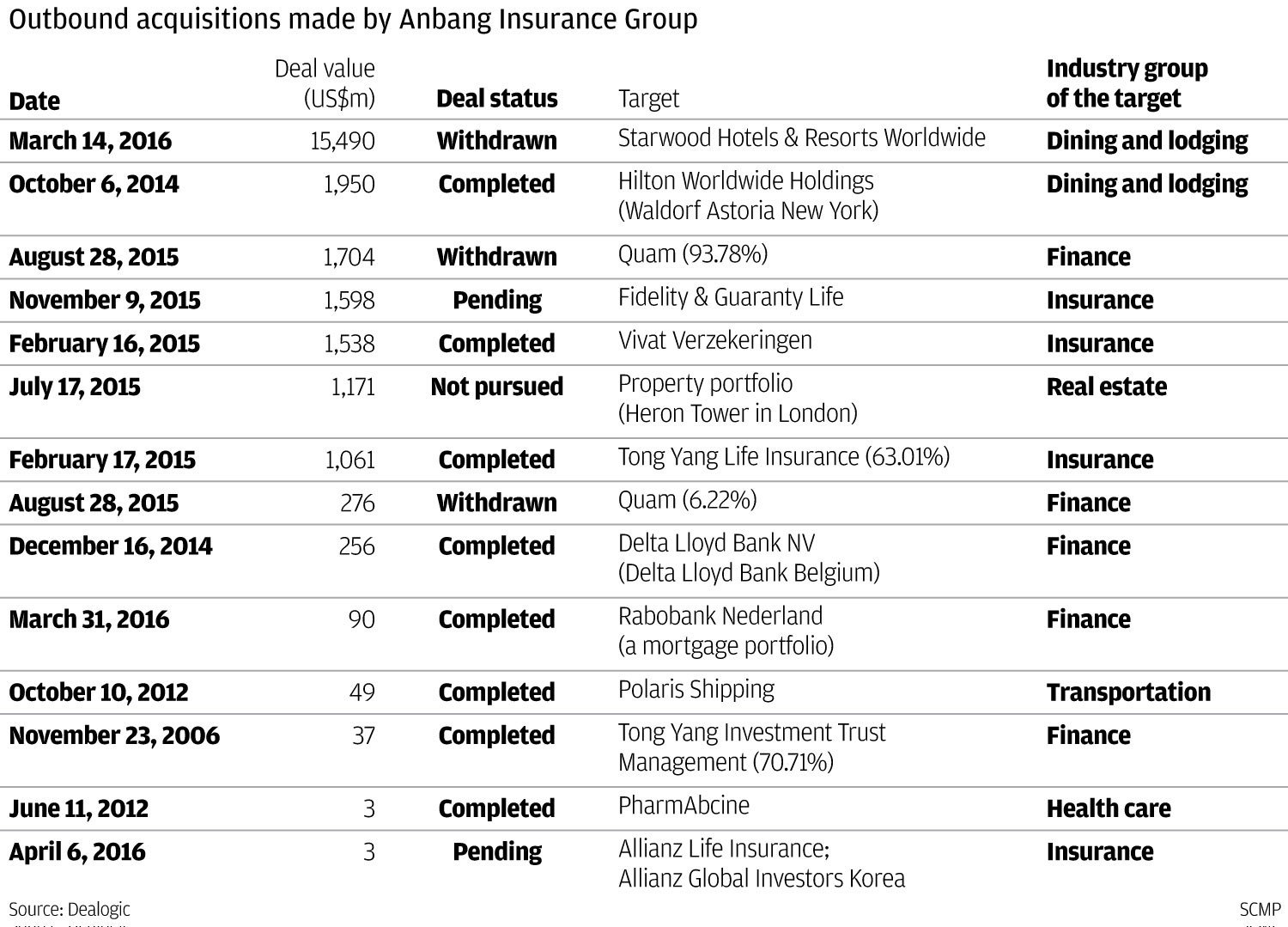

Anbang, whose chairman, Wu Xiaohui, was detained by police in June and remains MIA, has been characterized as an opaque, familial company. It initially made headlines in the U.S. when, in October 2014, it announced it was acquiring the Waldorf Astoria from Hilton for close to $2 billion. Other large hospitality-related deals made by Anbang included its $6.5-billion acquisition of the Strategic Hotels portfolio from Blackstone Group last year.

A Nice Run

This spate of overseas buying was not coincidence. Since 2012, regulation governing Chinese institutional investors changed to allow up to 15 percent of their portfolio allocated to foreign real estate assets. Before then, these portfolios could only hold 1 percent of total assets in foreign real estate.

According to Michael Bellisario, senior analyst with R.W. Baird, China's U.S. hospitality play is less about hotels and more about flight. "It's less about buying hotel real estate and more about getting capital out of their country, parking it in a gateway market and getting an asset that will hopefully appreciate in value," he said.

Bellisario said he was not entirely surprised by the declaration set forth in the initial Bloomberg article, but maybe the biggest takeaway being, as he said, "We just don’t know."

In his estimation, China has the ability "to flex muscle over its biggest corporations," and, not unlike any other country's economic and financial future, "billions of capital outflows are billions not being invested in their country," Bellisario said, unconvinced that Asian investment in hotels in U.S. gateway markets will curtail.

"Investing in these types of assets has a steep learning curve for these organizations," Daniel Voellm, managing partner of HVS Asia Pacific, told us earlier this year. "As a result, some firms were better positioned to capitalize in this new environment and executed deals quickly. The majority of institutional investors are looking to be active in this market given their allocation requirement and there will be continued activity with more experienced investment teams and faster execution cycles."

According to Voellm, hotels became attractive to Chinese investors, not only because of their potential returns, but because of their familiarity. "The focus on hotels and trophy assets is attributable to the inherent risk perception of these investors. For example, it is very difficult for a first-time investor in Beijing to discern the Bank of America Tower from say One Chase Manhattan Plaza in New York. While there are naming rights associated, tenants come and go and general built quality is difficult to ascertain. The brand name associated with a hotel, usually through a long-term contract, gives these investors confidence in the future performance and further bolsters their reputation by owning a well-known brand and even better, trophy asset.

Once Anbang acquired the Waldorf Astoria, Hilton signed a 100-year management contract.

Chinese companies up and through now continue to pour money into the hospitality arena. Beyond Anbang, companies such as HNA Group and China Life Insurance have allocated vast sums of capital. The former acquired Carlson and took a large position in Hilton, while China Life invested close to $2 billion in a Starwood Capital-owned select-service portfolio.

Rumblings in the U.S and Abroad

According to JLL, with $9.8 billion spent, investors from mainland China were the largest source of outbound capital into hotels in 2016. Across all investment classes, Chinese foreign direct investment in the U.S. totaled $45.6 billion in 2016.

Will these numbers keep up? Not likely. Earlier in the year, David Green-Morgan, JLL’s global capital markets research director, said, “We do believe that Chinese investors will continue to be major movers of capital into global real estate for many years to come, but a similar increase in 2017 may be challenging given the recent discussion about China monitoring its capital outflows."

And it's not just China keeping eye. In the U.S., some groups are petitioning the federal government to step in and thwart Chinese investment. In April 2016, Unite Here, which represents hotel workers, reached out to the Treasury, urging the Committee on Foreign Investment (CFIUS) to investigate Blackstone Group's $6.5-billion sale of Strategic to Anbang. It ultimately went through.

Others, reportedly, have not. According to a July Reuters report, CFIUS has "objected to at least nine acquisitions of U.S. companies by foreign buyers so far this year," a number that is characterized as large and indicative of the group becoming more risk averse under President Donald Trump.

Reuters reports that there have been 87 announced acquisitions of U.S. companies by Chinese firms so far in 2017, the highest on record and up from 77 deals in the corresponding period in 2016.

Beginning in late 2016, China began making it tougher for China-based companies to move money outside the country. A Wall Street Journal article reported that "China's foreign-exchange regulator has instructed banks to sharply limit how much companies move out of the country and into their other operations around the world."

Up until December 2016, it was reportedly simple for big companies to get $50 million worth of yuan or dollars in or out of China with minimal documentation or interference. According to the Wall Street Journal article, the cap is around $5 million. For its part, Beijing is blunting the impact of capital outflows that weaken the yuan.

Whether or not China's pullback is politically motivated remains to be seen, though President Trump has now intimated and reports suggest that he is gearing up to launch an investigation into whether Chinese trade practices are unfair, an investigation that could result in tariffs or other measures.

All this uncertainty is detrimental for one specific cohort: hotel sellers. What's an ownership's group play if they bring a hotel to market that is being chased by Chinese money? If China is the highest bidder, what is the certainty they can close? Do you take the second-highest bid from the likes of a real estate investment trust or private equity knowing they can, in all likelihood, close?

Bellisario views this as the biggest implication to come from the now nebulous cross-border transaction landscape. "If I’m a seller of real estate and my highest bidder is a Chinese buyer, it probably adds uncertainty, an extra layer to the transaction," he said. "The clearing price needs to be higher, because they are taking a risk to get a deal closed."

Bellisario cited REITs, such as Host Hotels or Sunstone Hotel Investors, whose balance sheets are public, "you know what they own," he said.

Sellers will be forced to ask themselves, "Do I sell to the second-highest bidder because the certainty of close is higher?" Bellisario said. "You don't want a deal to break down at the 1-yard line."