Hilton Worldwide has tweaked its full-year RevPAR forecast down in response to softening corporate travel and uncertain global economic picture.

Hilton expected RevPAR to grow 2 percent to 4 percent for 2016; it now is predicting a RevPAR gain between 1.5 percent and 2 percent. The numbers are alarming given that forecast agencies, such as STR, had predicted U.S. RevPAR to rise closer to 5 percent this year.

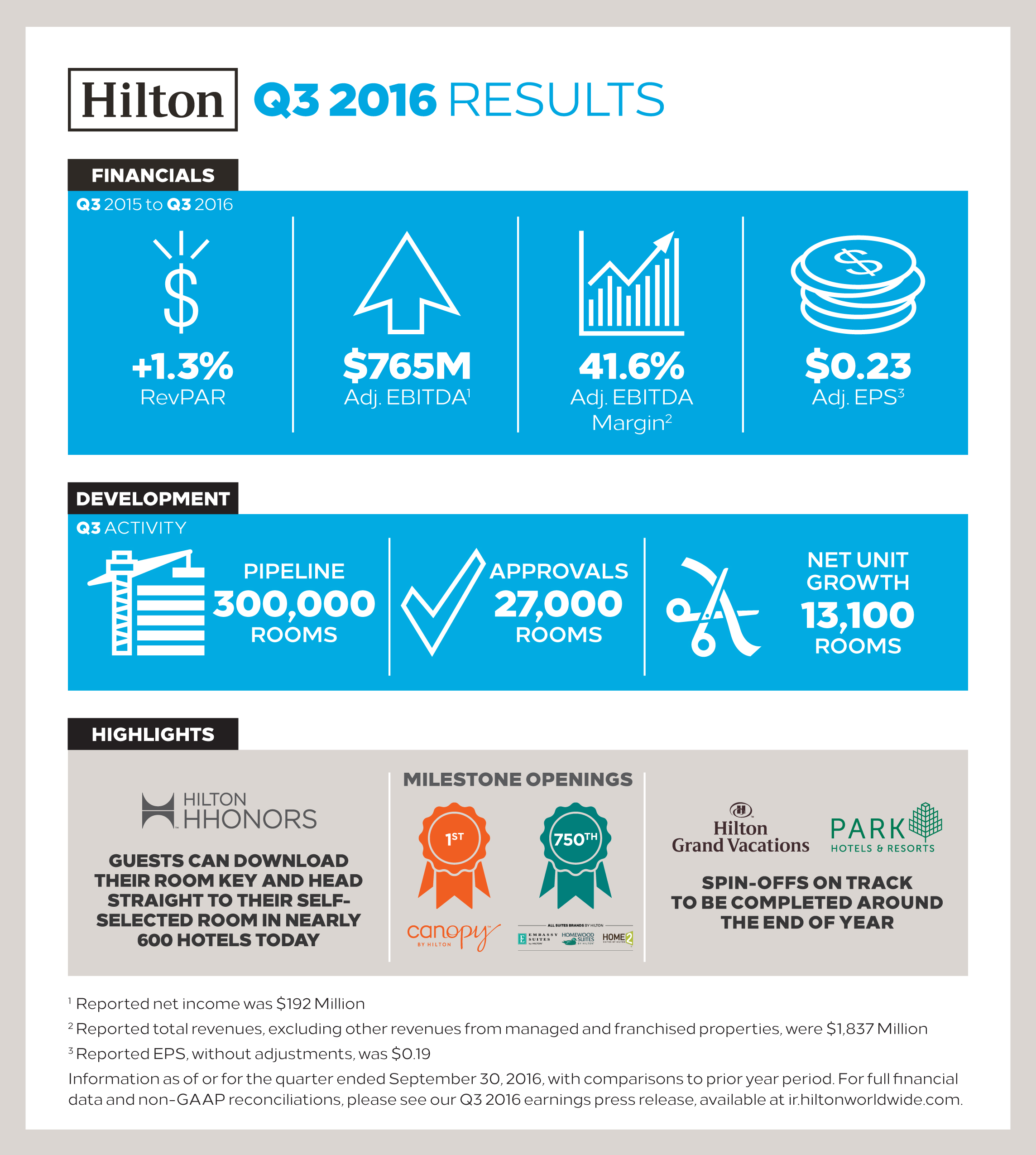

Net income was $192 million for the third quarter compared to $283 million at the same time last year. Management and franchise fees for the third quarter increased 7 percent from the same period in 2015 to $470 million.

RevPAR grew 1.3 percent driven entirely by rate in the quarter, due in part to softer transient demand, particularly in September, said Chris Nassetta, president and CEO of Hilton Worldwide.

The news comes as Hilton prepares to complete the spin-off transactions of its new REIT Park Hotels & Resorts and Hilton Grand Vacations by the end of the year.

Nassetta focused on the positive in his prepared statement: "Even with a macroeconomic environment that continues to underperform expectations, we delivered adjusted EBITDA and EPS, adjusted for special items, within our guidance ranges and continued to increase our global share of development activity this quarter," he said. "We approved deals for 27,000 new rooms in 22 different countries on five continents and opened over 14,300 rooms this quarter. Our accelerating, capital-light growth is driven by all of our clearly defined brands, with each of our brand segments at record pipelines. Our brands currently represent 22 percent of all rooms under construction globally, or nearly five times their current share of room supply."

It's Vague Out There

Still, though the current operating environment can't be characterized as bleak, it's awfully tenuous and dependent on factors outside hospitality's control, such as GDP growth, job growth and the broader global economy. Those three factors, coupled with what feels like an interminable election cycle, is causing an out-our-control sentiment throughout the industry.

"The lodging lodging cycle aligns with the business cycle," Nassetta said, adding that he believes—is hopeful—that GDP will be higher, there will be incremental job growth and, "with the election behind us," more certainty by companies on future plans and strategy.

"I talk to CEOs, our customers, and there is a view right now, exacerbated by the election cycle, that everyone is nervous—that there is broad uncertainty. And that impacts CEOs loosening purse strings, making hiring and spend decisions. When people have more certainty, they do want to make decisions to invest, travel and hire to drive growth. But this unusual election cycle has slowed down the economy more than I've seen. There is an aura of uncertainty. People are waiting."

On the good side, Hilton said corporate negotiated rates, which are in the early stages of negotiation, look to increase between 2 percent and 3 percent based off of the high occupancies of 2016. Additionally, Nassetta said that 70 percent of group bookings are already on the books for next year.

Organic net unit growth, Nassetta said, should increase as high as 7 percent next year, and that's with "no capital output," Nassetta said.

China Calling

Hilton's Q3 call comes just days after the news that China's HNA Group was acquiring 25 percent of Hilton, which winds down Blackstone Group's ownership stake in the company to 21 percent. Nassetta called the deal a win for all parties.

Hotel companies are seeking any foothold to grow their business in China, the fastest-growing lodging market and outbound market. This deal, Nassetta said, accelerates that very idea.

"We spent time with HNA in the lead up to the announcement," he said. "We believe there are some compelling reasons why this is beneficial. They are big time in travel and tourism, with an airline and millions of loyal members. They are well respected in China and globally.

"The idea is to we have our customer base, they have their base, and there is not much overlap between our customer base and theirs, so there is the opportunity to connect those bases. It's mutually beneficial."

HNA also has reach into China's debt and financial markets, another benefit for Hilton. "We are dependent on third-party capital and the better we have access to it, the more beneficial," Nassetta said, adding that the deal also helps with Hilton's overhang issue.

On the development front, Hilton approved 27,000 new rooms for development during the third quarter, bringing year-to-date approvals to 77,000 rooms; grew the development pipeline 15 percent from 2015 to 1,898 hotels, consisting of 300,000 rooms; and net unit growth was 13,100 rooms in the third quarter, representing a 7-percent growth in managed and franchised rooms from 2015.

Hilton continues to push its Tru brand, and Nassetta promoted the brand's shorter gestation period in regard to build-out and ease of finance. By the end of 2016, Nassetta said there would be as many as 20 Tru hotels under development.

Nassetta grew noticeably prickly during the call when one analyst asked him to comment now that Marriott's deal for Starwood had closed. The two companies have competing growth strategies: Marriott by M&A, Hilton organically.

"We are confident in our strategy, with our pure-bred brands and premium market share," Nassetta said. "We are driven by organic net unit growth. Others have taken a different paths. We chose our strategy and remain confident.

"Scale does matter and I think we have it. Our 1.1 million rooms gives us scale. What Marriott does—I'm not going to comment. Ask them."